Rystad forecasts bleak outlook if OPEC+ fails to agree on deeper cuts

Barring additional oil production cuts by OPEC in 2020, Norwegian energy intelligence company, Rystad Energy, forecasts a substantial build of global crude stocks and a corresponding drop in oil prices.

A showdown is taking place in Vienna as OPEC countries plus Russia will gather in the Austrian capital on 5-6 December to discuss oil output levels in 2020.

“We have a clear message to the OPEC+ countries: A ‘roll-over’ of the current production agreement is not enough to preserve a balanced market and ensure a stable oil price environment in 2020,” says Bjørnar Tonhaugen, head of oil market research at Rystad Energy.

“The outlook will be bleak if OPEC+ fails to agree on additional cuts.”

According to Rystad Energy’s estimates, the global oil market will be fundamentally oversupplied to the tune of 0.8 million barrels per day (bpd) in the first half of 2020.

Empirical evidence has demonstrated that a 1 million bpd surplus of oil can be expected to cause an oil price decline of around 5% per month, implying a potential drop of 30% over six months.

“If OPEC and Russia don’t extend and deepen their cuts, we could see Brent Blend dip to the $40s next year for a shorter period,” Tonhaugen said.

“In order to ensure a balanced market, our research indicates that OPEC would need to reduce crude production to 28.9 million bpd – a drop of 0.8 million bpd from the level seen in the fourth quarter of 2019-levels – given our forecast for demand, non-OPEC supply and the impact of new IMO 2020 regulations on global crude runs,” Tonhaugen added.

New shipping fuel regulations, the so-called IMO 2020 effect, are expected to create more demand for crude oil in the near-term. However, if the actual effect of the IMO rules on crude demand turns out to be zero the “call on OPEC” – the amount of OPEC oil needed to meet demand – drops by 1.9 million bpd year-on-year to 28.3 million bpd.

“Despite decent cut compliance from the group as a whole and large involuntary declines in Iran and Venezuela this year, OPEC’s current crude production of about 29.7 million bpd is far above the ‘call’ for 2020. Alas, without deeper cuts taking effect in January 2020, large global implied stock builds are on the cards,” Tonhaugen remarked.

Rystad Energy sees three alternative OPEC+ decision scenarios:

**Base case: Extension of current production cuts to June 2020. Global oil market will be oversupplied to the tune of 1.2 million bpd in 2020. Significant oil price correction, possibly down to the low $40s for a short period, is likely.

**Deeper cuts: Additional cut of 0.75 million bpd on top of the 0.3 million bpd in the extension scenario would reduce the supply overhang and ensure stable prices.

**No deal/market share war: A ramp-up to maximum production capacity in all countries could have devastating effects. With potential stock builds of 2.3 million bpd, oil prices could fall below $30/bbl – lower than during the previous lows of 2016. Such a scenario would be devastating for the forward curve structure as potential stock builds would be larger than what we have observed historically.

Rystad Energy finds that OPEC+ as a whole has cut oil production by 2.6 million bpd year-to-date, compared to October 2018 reference levels and the cut target of approximately 1.2 million bpd. The additional 1.4 million bpd of “cuts” are owed entirely to involuntary declines from Iran and Venezuela, both of which are exempt from the agreement. Saudi Arabia has led the group’s compliance by cutting 870,000 bpd in 2019, or 2.7 times its target cut of 322,000 bpd.

“Saudi Arabia has signaled that it seeks stricter compliance by other producers and is no longer willing to shoulder the burden of sub-compliance by others, such as Russia, Iraq and Kazakhstan, which have all failed to reach 100% compliance with their target cuts,” Tonhaugen said.

The challenge for OPEC+ is the strong supply growth elsewhere in the world. Rystad Energy forecasts a supply growth of 2.6 million bpd year-on-year in 2020, led by US shale, Norway and Brazil against weak global demand growth of only 1.0 million bpd year-on-year. Rystad Energy forecasts that non-OPEC non-US supply will grow 1.2 million bpd year-on-year in 2020, OPEC estimates this number at 0.6 million bpd year-on-year.

Saudi Arabia together with other OPEC members and Russia have decided on deeper production cuts for the first quarter of next year as part of an attempt to prevent oversupply and support oil prices.

Entrance of the OPEC Headquarter in Vienna; Source: Wikimedia; Author: Vincent Eisfeld – under the CC BY-SA 4.0 license

Following a meeting in Vienna last Friday, the 7th OPEC and non-OPEC Ministerial Meeting decided for an additional adjustment of 500 tb/d to the adjustment levels as agreed at the 175th Meeting of the OPEC Conference and 5th OPEC and non-OPEC Ministerial Meeting. These would lead to total adjustments of 1.7 mb/d.

In addition, several participating countries, mainly Saudi Arabia, will continue their additional voluntary contributions, leading to adjustments of more than 2.1 mb. This additional adjustment would be effective as of January 1, 2020, and is subject to full conformity by every country participating in the ‘Declaration of Cooperation’ (DoC).

The DoC was reached on December 10, 2016, between OPEC and non-OPEC producing countries.

Reuters reported on Friday that, of the 500,000 bpd additional cuts, OPEC would shoulder 372,000 bpd and non-OPEC producers an extra 131,000 bpd.

According to a Friday statement by OPEC, participants reaffirmed their continued focus on fundamentals for a stable and balanced oil market, in the interests of producers, consumers, and the global economy.

The meeting emphasized the vital support and commitment of all participating countries in the DoC to build on the success achieved thus far, through each individual country adhering to their voluntary production adjustments and in supporting the Charter of Cooperation between Oil Producing Countries.

In order to observe the fair, timely and equitable implementation of the agreement, the Joint Ministerial Monitoring Committee was requested to continue to monitor its implementation and report back to the meeting, supported by the Joint Technical Committee and the OPEC Secretariat.

The 18th Meeting of JMMC will be held during the first week of March 2020 in Vienna, Austria, with an OPEC and non-OPEC Ministerial Meeting on March 6, 2020. The meeting decided that an OPEC and non-OPEC Ministerial Meeting also will convene in Vienna, Austria, on June 10, 2020.

WoodMac: March commitment could reduce its supportive impact

Ann-Louise Hittle, Wood Mackenzie’s vice president Macro Oils, said: “The group is taking a highly proactive approach to managing the market and will not commit to restraint beyond March 2020, when both a joint ministerial meeting and an extraordinary meeting will be held in the first week of the month.

“Russia has gained approval for its request to remove condensate from its quota. It will make an additional cut of 70,000 b/d beyond its current agreed cut of 300,000 b/d.

“Russia’s energy minister Alexander Novak confirmed the country’s commitment to cooperate with OPEC to balance the market.

“The new Saudi Energy Minister, Prince Abdul Aziz, was adamant that all those in the agreement must adhere and not leave the burden on Saudi Arabia.”

She added: “The fact the agreement runs to March could reduce its supportive impact on the market. However, the proactive, short-term management of the market OPEC+ is signalling is supportive overall to the outlook for 2020 and should avoid a significant downturn in prices.

ExxonMobil sees 3Q profit fall 49% on lower oil prices

Oil and gas behemoth ExxonMobil reported a 3Q net profit of ~$3.2 billion, a 49 percent fall vs ~$6,25 billion a year ago.

Liza Destiny FPSO on its way to ExxonMobil’s Liza field in offshore Guyana; Source: Hess

The company cited lower prices, and higher growth-related expenses in the upstream division, lower margins in the Chemical and Downstream businesses as some of the reasons behind the drop in earnings. Brent crude averaged $62 in the third quarter of 2019, down from $75 in the third quarter of 2018.

Exxon’s production grew three percent from the third quarter of 2018 to 3.9 million barrels per day. Excluding entitlement effects and divestments, liquids production increased 4 percent driven by Permian Basin growth, while natural gas volumes increased 1 percent.

“Liquids volumes were in line with the second quarter, with U.S. unconventional growth offsetting the base decline. Natural gas volumes were down 1 percent. Permian unconventional development continued with production up 7 percent from the second quarter and more than 70 percent from the third quarter of last year,“ ExxonMobil said.

In the offshore space during the quarter, the company announced another oil discovery on the Stabroek block offshore Guyana at the Tripletail-1 well, adding to the previously announced resource estimate of more than 6 billion oil-equivalent barrels.

The Liza Destiny floating production, storage, and offloading vessel arrived offshore Guyana, targeting first oil at the Liza Phase 1 development by December 2019. ExxonMobil estimates gross production from the Stabroek block will exceed 750,000 oil-equivalent barrels per day by 2025.

In Europe, ExxonMobil signed an agreement with Vår Energi AS for the sale of its non-operated upstream assets in Norway for $4.5 billion as part of its previously announced plans to divest approximately $15 billion in non-strategic assets by 2021.

“We are making excellent progress on our long-term growth strategy,” said Darren W. Woods, chairman, and chief executive officer. “Growth in the Permian continues to drive increased liquids production and we are ahead of schedule for first oil in Guyana. The value of our position in Guyana improved further this quarter with an additional discovery, our fourth this year. We are also making good progress on our advantaged investments in the Downstream and Chemical.

“This quarter, we started production at our new high-performance polyethylene line in Beaumont. The competitiveness of our portfolio was further enhanced with the divestment of non-strategic assets, reaching almost a third of our 2021 objective of $15 billion.”

Report: Oil prices rise over U.S. – Iran tensions after U.S. drone shot down

Oil price rose Friday over tensions between the U.S. and Iran, following reports on Thursday that Tehran had shot down a U.S. drone in what the U.S. said was international airspace. Tehran claims the drone violated Iran’s airspace.

File photo of a RQ-4 Global Hawk unmanned surveillance and reconnaissance aircraft. (U.S. Air Force photo)

The U.S. Central Command said that “a U.S. Navy Broad Area Maritime Surveillance (or BAMS-D) ISR aircraft was shot down by an Iranian surface-to-air missile system while operating in international airspace over the Strait of Hormuz at approximately 11:35 p.m. GMT on June 19, 2019.

“Iranian reports that the aircraft was over Iran are false. This was an unprovoked attack on a U.S. surveillance asset in international airspace,” it said on Thursday.

The drone incident follows last week’s attack on two oil tankers near Iran’s coast for which the U.S. has blamed Iran, and which Iran has denied.

The tankers were attacked near the Strait of Hormuz, through which a fifth of the globally consumed oil is shipped, and which the U.S. Energy Information Administration on Thursday labeled as the “world’s most important oil transit chokepoint.”

Reuters on Friday reported that Brent Crude had risen to over $65 a barrel over the tensions and potential conflict, with the news agency citing Iranian sources who claim that U.S. president Donald Trump had sent them a warning of an imminent U.S. attack on Iran. The news agency also cited a New York Times report in which it has been claimed that Trump had approved military strikes but then pulled back from launching them.

Following the reports of a U.S. drone being struck down, Trump tweeted: ”Iran made a very big mistake.”

However, Trump then on Friday in a series of Tweets confirmed the U.S. was “cocked and loaded to retaliate,” but he stopped the strike “10 minutes before” as he had been informed 150 people would die, which he felt was “not proportionate to shooting down an unmanned drone.”

Responding to claims that Iran had shot down the U.S. drone in international waters, Iran’s Foreign minister Javad Zarif said on Thursday via twitter: “At 00:14 US drone took off from UAE in stealth mode & violated Iranian airspace. It was targeted at 04:05 at the coordinates (25°59’43″N 57°02’25″E) near Kouh-e Mobarak. We’ve retrieved sections of the US military drone in OUR territorial waters where it was shot down.”

“The US wages #EconomicTerrorism on Iran, has conducted covert action against us & now encroaches on our territory. We don’t seek war, but will zealously defend our skies, land & waters. We’ll take this new aggression to #UN & show that the US is lying about international waters,” Zarif said.

By economic terrorism, Zarif means the U.S. Economic Sanctions which Trump reimposed on Iran after he had in May 2018 terminated the U.S. participation in the Iran nuclear agreement devised in 2015 to curb Iran’s nuclear weapons development capacity, labeling it “one of the worst and most one-sided transactions the United States has ever entered into,” much to a dismay of the international community, as Iran had stuck to its part of the agreement.

The sanctions on Iran’s oil sector, which kicked in November 2018, have targeted the Iranian crude oil sales, and also countries who buying Iranian oil with the aim reportedly to bring Iran’s production to zero, with Trump saying that anyone doing business in Iran “will NOT be doing business with the United States.”

Pressure on buyers

Credit rating agency Fitch late in May said that the pressure on buyers of Iranian oil had intensified and the country was likely to reduce exports.

“This is due to the US not renewing waivers to continue to purchase crude from Tehran for China, India, Italy, Greece, Japan, South Korea, Taiwan and Turkey. This is likely to reduce spare capacity elsewhere in the market and has already caused price volatility. It also increases the chances of oil prices rising in the short term.”

“We believe it is unlikely that Iran’s exports will fall to zero as some countries, notably China, continue to buy oil from it despite the removal of waivers. However, we assume export volumes could halve, compared to around 1 million barrels per day (MMbpd) at the beginning of the year, as Italy, Greece and Turkey have stopped buying Iranian crude,” Fitch said in a report on May 24.

U.S. Energy Information Administration estimates that 76% of the crude oil and condensate that moved through the Strait of Hormuz went to Asian markets in 2018.

“China, India, Japan, South Korea, and Singapore were the largest destinations for crude oil moving through the Strait of Hormuz to Asia, accounting for 65% of all Hormuz crude oil and condensate flows in 2018,” the EIA said on Thursday.

World’s most important oil transit chokepoint

As said earlier, the U.S. Energy Information Administration on Thursday released a report in which it said that the Strait of Hormuz was “the world’s most important oil transit chokepoint”

“The Strait of Hormuz, located between Oman and Iran, connects the Persian Gulf with the Gulf of Oman and the Arabian Sea. The Strait of Hormuz is the world’s most important oil chokepoint because of the large volumes of oil that flow through the strait. In 2018, its daily oil flow averaged 21 million barrels per day (b/d), or the equivalent of about 21% of global petroleum liquids consumption,” U.S. EIA said, warning that the inability of oil to transit a major chokepoint, even temporarily, can lead to substantial supply delays and higher shipping costs, resulting in higher world energy prices.

The EIA said that while most chokepoints can be circumvented by using other routes that add significantly to transit time, “some chokepoints have no practical alternatives.”

“There are limited options to bypass the Strait of Hormuz. Only Saudi Arabia and the United Arab Emirates have pipelines that can ship crude oil outside the Persian Gulf and have the additional pipeline capacity to circumvent the Strait of Hormuz. At the end of 2018, the total available crude oil pipeline capacity from the two countries combined was estimated at 6.5 million b/d. In that year, 2.7 million b/d of crude oil moved through the pipelines, leaving about 3.8 million b/d of unused capacity that could have bypassed the strait,” EIA said.

Fitch sees Brent averaging $65 in 2019

In a report on Monday – so, before the drone incident – Fitch said that increased geopolitical tensions and economic uncertainty are likely to contribute to oil price volatility, but its year-average base-case expectations remained unchanged.

Fitch said in the report: “The toughened sanctions against Iran, production declines in Venezuela and the conflict in Libya contributed to Brent price recovery to around USD75/bbl by end-April from USD50/bbl at end-2018. However, the price fell to USD60/bbl in early June due to deteriorating expectations for global economic growth and increased trade war risks. We expect the global economy to decelerate from 3.2% in 2018 to 2.8% in 2019 and 2.7% in 2020.

Nevertheless, we expect OPEC+ to continue to manage supply to avoid large supply-demand imbalances. We believe that the OPEC+ deal will be extended until at least the end of this year, though its parameters could change. As a result, we expect the market to stay broadly in balance, and assume annual average prices will remain in line with our existing base-case assumptions. Year-to-date average prices (Brent: USD66/bbl) are consistent with our assumption of USD65/bbl for 2019.

Many large Middle Eastern producers (such as the UAE and Kuwait) should be able to balance their budgets comfortably under Fitch’s base case assumptions for 2019-2020, except Saudi Arabia, the “swing” producer. Saudi Arabia requires Brent to be priced above USD80/bbl, hence its decision to produce below its OPEC+ quota, putting upward pressure on crude prices.

In the longer term we assume average prices to moderate to USD57.5/bbl for Brent and USD55/bbl for WTI as OPEC+ policies may become less efficient over time. The differential between Brent and WTI will narrow as transportation constraints gradually ease. We expect US upstream companies to remain profitable at these price levels, assuming the current cost base and achieved efficiency gains. We expect production growth in the US to meet most of the additional global demand in the next few years as it does now. At the same time the responsiveness of US shale to current prices makes the scenario of oil prices falling consistently below USD50/bbl significantly less likely.”

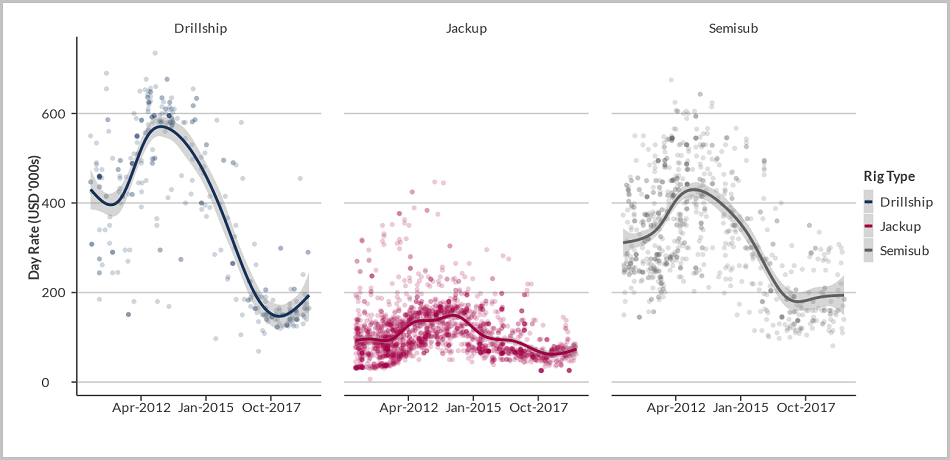

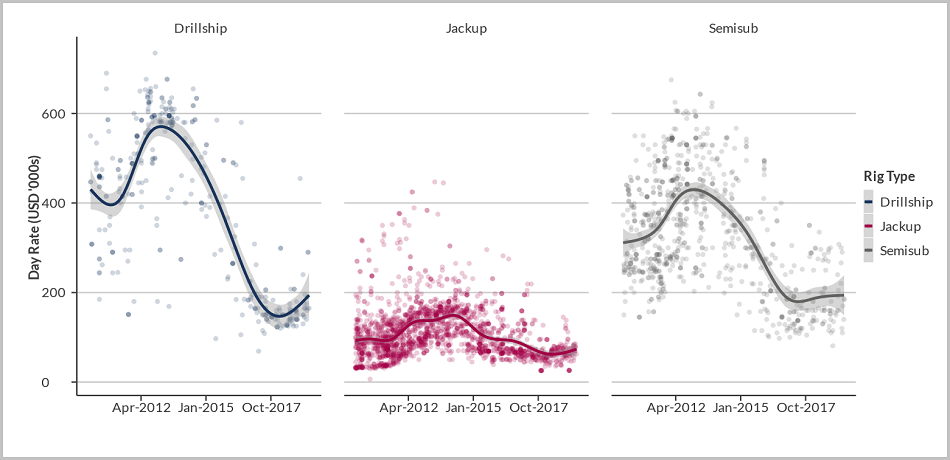

There have been improvements over the past 18 months, according to Westwood’s Matt Adam, with 460 mobile offshore drilling units (MODUs) working globally last month, the highest level of activity since May 2016, when 466 rigs were in service.

Over the same period, supply has decreased due to 207 MODUs being withdrawn from the fleet, although 101 newbuilds have also been delivered.

Global use of the MODU fleet is now at 59%, 12 percentage points higher than the low point of February 2017, and day rates for new contract awards are rising, notably in niche markets such as the Norwegian North Sea.

The rig market as a whole appears to have emerged from one of its worst ever downturns and Adams expects demand to continue to increase as operators work through a backlog of delayed projects, while at the same time more aging, under-spec rigs are retired.

So, there is room for cautious optimism, although the offshore rig market seems unlikely to return to the heights of the previous up-cycle, Adams concluded.

06/17/2019

Historic leading day rates by rig type and date of award, Jan. 1, 2010- June 1, 2019. Line is Generated using GAM Smoothing.RigLogix / RigOutlook

Rystad: No room for OPEC+ to increase output for the rest of 2019

The OPEC+ countries will not be able to increase their collective oil production levels in the second half of 2019 without having a detrimental effect on oil prices, according to Norwegian oil and gas intelligence firm Rystad Energy.

Even though a production increase is off the cards without influencing prices, Rystad Energy said on Tuesday that the production cuts required by OPEC+ to support prices need not be as much as 1.5 mbpd.

According to the intelligence firm, that is contrary to what traditional supply-demand balances suggest, owing to a tight market for medium and heavy barrels and the fast-approaching shipping fuel changes known as IMO 2020, which are expected to cause an increase in crude demand.

Disappointing global demand and strong production growth in the U.S. are also weighing on OPEC+’s decision, which may be postponed to early July.

Ahead of the 6th OPEC Ministerial Meeting in Vienna, Austria, Rystad Energy’s chief oil market analyst Bjørnar Tonhaugen said: “We expect crude demand to accelerate thanks to the upcoming IMO 2020 regulations later this year, and OPEC will likely not have to cut production as much as the call on OPEC suggests.

“Having said that, there will not be room for the cartel to increase output for the rest of 2019 in our view.”

Rystad Energy’s supply-demand forecast suggests that the so-called call on OPEC production will decline by 1.5 million bpd to 29.0 million bpd from the second quarter to the fourth quarter of 2019.

OPEC+, which consists of OPEC countries plus Russia and several other supportive producers, account for nearly 49 million of the 84 million bpd of global crude and condensate production expected to be produced on average in 2019.

“We expect non-OPEC+ production to grow by 1.9 million bpd year-on-year in 2019, driven by the continued rise of the U.S. shale industry, whereas global demand is expected to grow only by between 1.1 million and 1.2 million bpd year-on-year.

“In other words, as non-OPEC+ adds more supply than global demand is increasing by, OPEC+ will still be pressured to manage production to balance the global market,” Tonhaugen added.

A forecast by Rystad Energy stated that U.S. oil production would grow by 1.6 million bpd y/y in 2019, with monthly production reaching 13.4 million bpd by December 2019. The brunt of the supply growth comes from the Permian Basin, the prolific shale play in Texas and New Mexico.

U.S – China tariff war

It is worth noting that Brent benchmark crude prices have shed more than 13 dollars per barrel since reaching a recent peak in May. Fear of a possible trade war between the U.S. and China over tariffs also dampen the outlook.

“However, the fears about the impact of recent tariffs on global oil demand growth are overblown,” Tonhaugen said.

“We believe the current oil price weakness is fueled more by expectations of faltering trade prospects and a worsening global economy, rather than by the direct effect of new and existing tariffs on oil demand.”

Rystad Energy’s analysis suggests that if the U.S. and China proceed with another round of tariff hikes, covering all their respective trade volumes, global oil demand growth could fall by 100,000 bpd in 2019 and 400,000 bpd in 2020.

This is the direct result of lower trade volumes for the U.S. and China, as well as for China’s main Asian trade partners such as Japan, South Korea, and the EU.

“The downside may be even greater if the global economy, especially the Chinese economy, continues to slow. With this in mind, we believe the market is currently bracing for a greater impact than what current tariffs will deliver,” Tonhaugen concluded.

Worldwide offshore rig count in May up by 43 rigs year-over-year

The worldwide offshore rig count in May 2019 dropped by 11 units sequentially but was up 43 rigs year-over-year, according to monthly rig count reports by Baker Hughes, a GE company (BHGE).

BHGE splits its rig counts into international and North America rig counts, which combined make the worldwide rig count.

Baker Hughes said on Friday that the international rig count for May 2019 was 1,126, up 64 from the 1,062 counted in April 2019, and up 159 from the 967 counted in May 2018. It is worth noting that the international rig count now includes active drilling rigs in the Ukraine.

The international offshore rig count for May 2019 was 240, down 11 from the 251 counted in April 2019, and up 42 from the 198 counted in May 2018.

Regionally, Asia Pacific had the highest number of offshore rigs in May totaling 90, down 9 from April 2019 and up 9 from 81 in May 2018.

The Middle East region held the second place in the number of offshore rigs during May totaling 54, down 2 rigs from April 2019 and up 6 from 48 counted in May 2018.

Next up was Europe with 44, then Latin America with 30, and finally Africa with 22 offshore rigs in May 2019.

In North America, the offshore rig count in May 2019 totaled 24, which was the same number from the month before and up 1 from 23 counted in May 2018.

The worldwide rig count for May 2019 was 2,182, up 42 from the 2,140 counted in April 2019, and up 86 from the 2,096 counted in May 2018.

The worldwide offshore rig count for May 2019 was 264, down 11 from 275 in April 2019 and up 43 from 221 in May 2018.

Industry watchers weigh in on the idea of a complete collapse this year.

Fitch Solutions does not expect to see Venezuela’s oil output collapse and go to zero in 2019, according to the company’s head of oil and gas analysis, Joseph Gatdula.

The Fitch Solutions representative conceded that the oil sector in the country is showing “accelerating signs of stress” but said the company believes Venezuela will be able to sustain between 300,000 and 500,000 barrels per day (bpd) of exports, “mainly with Russia and China”.

Echoing Fitch Solutions’ view, the director of Apex Consulting Ltd, Muktadir Ur Rahman, revealed that his company does not expect a “complete collapse” of Venezuela’s oil sector this year either. The director added, however, that in the absence of a political solution, his company believes further “significant” production falls are inevitable.

According to Rahman, Venezuela’s oil output could fall to around 500,000 bpd by the end of 2019 in a worst-case scenario.

“On the other hand, it is possible to arrest this decline somewhat and in a relatively short time frame, if [the] political situation improves in 2019,” Rahman told Rigzone.

“This is because it would still be quite easy for the international oil companies (IOC) to bring production in the Orinoco basin back to its pre-crisis level once the power situation improves and it becomes easier for them to import diluents necessary to operate the upgraders,” he added.

“However, it would be much more challenging for Venezuela to improve the production of its ageing fields elsewhere, where lack of investment and years of mismanagement have caused production to decline very steeply, and in some cases, irreversibly,” Rahman continued.

Further exploration and development of Venezuela’s oil reserves would be crucial to bringing the country’s overall oil production back to its pre-crisis level, according to Rahman, who said to achieve this, Venezuela would have to partner up with IOCs.

“Given Venezuela’s recent history, this may not be an easy task, even though it has one of the largest oil reserves in the world,” Rahman said.

Upheaval Beyond 2019

According to Abhishek Kumar, head of analytics at Interfax Energy in London, Venezuela’s political and economic upheaval will continue to adversely affect the country’s oil sector in 2019 and beyond.

Kumar stated that recession and hyperinflation in Venezuela are set to continue for the rest of this decade and the Interfax representative said this will limit the government’s ability to invest in the country’s upstream “at a time when IOCs have already lost confidence in Venezuela’s oil sector”.

The country’s oil industry has had a checkered history since the heady period of 1970, according to PwC’s Director of Research, Adrian Del Maestro. According to Rahman, many would say Venezuela’s oil sector has been “crumbling for quite some time now”.

The Organization of Petroleum Exporting Countries’ (OPEC) latest monthly oil market report shows that, based on secondary sources, Venezuela’s oil output was 768,000 bpd in April. The country’s oil output stood at 740,000 bpd in March and 1.02 million bpd in February, based on secondary sources, according to OPEC’s report.

Venezuela’s oil production, based on direct communication, was 1.03 million bpd in April, 960,000 bpd in March and 1.43 million bpd in February, OPEC’s latest report revealed. Venezuela was one of the founding countries of OPEC back in September 1960. The Islamic Republic of Iran, Iraq, Kuwait and Saudi Arabia were the other founding countries of OPEC.

In a Twitter statement posted on January 23, U.S. President Donald Trump announced that he had officially recognized Juan Guaido as the interim president of Venezuela and labeled the Maduro regime as “illegitimate”. During the same month, Nicolas Maduro was sworn in for a second term.

Recent years’ M&A activity hasn’t quite lived up to the industry’s expectations. Experts take a look at some of the reasons why.

When markets start to stabilize, more mergers and acquisitions (M&A) activity is expected.

So far that hasn’t been the case for the oil and gas industry.

“Traditionally, price volatility has resulted in lower valuations, but currently, the bigger impact is really just lack of capital and lack of risk appetite around assets, particularly in upstream,” Brooks Shughart, managing director for private equity frim First Reserve, said recently during the Mergermarket Energy Forum in Houston. “The upstream space has not generated returns in any commodity price environment over the last 10 years.”

Expectations of massive consolidation after the downturn didn’t bear much fruit.

“Last year was supposed to be the year of consolidation. Well, it didn’t happen,” said Terry Padden, director for Simmons Energy, an energy investment banking firm. “Even prior to that, we were expecting consolidation coming out of the downturn, and it didn’t really happen in a big way.”

Padden said oilfield service companies in particular are in desperate need of consolidation.

“Over the past year, we’ve started to see upstream consolidation, such asthe Anadarko deal,” he said. “That gives a lot of the smaller service companies pause because you don’t need to be bigger just to be efficient. You need to be bigger to have relevance.”

Patrick McWilliams, partner for private equity firm NGP, shared his view from a slightly different lens.

“We’re trying to find really great talent, so we spend a lot of time talking to executives of the great operating companies,” said McWilliams. “When you build those relationships, you start gaining insight into the mentality of how the companies are being run. You look under the hood of what’s going on in the boardrooms and it’s just really bad misalignment.”

McWilliams said, as a private company, they spend a lot of time trying to get investors aligned with management teams to really focus on driving shareholder value.

“It’s hard to do and we don’t always get it right,” he said. “And it’s really hard to do in the public environment. What could make obvious sense in a spreadsheet may not necessarily make obvious sense from a social dynamic perspective.”

McWilliams said the industry has been essentially sitting around for about 10 years saying it needs more corporate to corporate M&A.

“Through five years of ‘lower for longer,’ enough pain has set in … now it’s ‘okay, we have to scale, we have to create synergies and we have to drive value,’” he said. “Are we really at that tipping point where we’re going to see a lot of it? Who knows? But we’re starting to see more of it.”

“Weatherford is a classic example of a company that was built through 100 percent M&A – aggressive M&A,” said Padden. “Adding a lot of pieces together, there were some very good business lines in Weatherford, but there were a lot of things that probably should not have been pursued.”

Things can turn from a fairytale to a nightmare.

“If you don’t manage it correctly, you find that, like with all big companies … the best people who work with Weatherford are gone,” Padden said. “Business lines have gone to competing companies in many cases, so it’s probably that the company honed in on M&A and lost focus. [Weatherford] got to scale through a strategy that ultimately didn’t work and then when you lose good people – even if you’ve got a good business – you’re not going to be able to keep that going.”

About nine in 10 U.S. shale companies are tremendously overspending, according to new analysis by Rystad Energy.

US Shale Companies are Burning through Cash

Just about 10 percent of U.S. shale companies had a positive cash flow in the first quarter of 2019, meaning the majority of companies are burning through cash, according to energy research firm Rystad Energy.

After studying the financial performance of 40 U.S. shale companies, Rystad found just four reported a positive cash flow balance in 1Q 2019. This is down from the recent norm of 20 percent.

Total S.A. saw its cash flow from operating activities (CFO) fall from $14 billion in 4Q 2018 to $9.9 billion in 1Q 2019.

“That is the lowest CFO we have seen since the fourth quarter of 2017,” said Alisa Lukash, senior analyst on Rystad Energy’s North American Shale team. “The gap between CAPEX and CFO has reached a staggering $4.7 billion. This implies tremendous overspend, the likes of which have not been seen since the third quarter of 2017.”

Shale companies will be forced to cut CAPEX if they receive no additional funding or debt refinancing.

But, according to Rystad, no U.S. shale company has made a public offering since the steep decline in oil prices late last year, marking the longest gap in public capital issuance since 2014.

“Recently released data, which confirmed dismal first quarter earnings, only served to cement negative market sentiment,” Lukash said. “While shale operators continue to focus on improving capital efficiency, investors are putting the industry under extreme pressure, leaving no room for undisciplined spending in 2019.”

But with shale operators ramping up production, Rystad expects a significant increase in CFO in second quarter as oil prices improve.

“Larger diversified operators, which have multiple cash generating engines and are more resistant to volatile commodity prices, will be especially poised to open up to acquisition of new acreage,” Lukash added.